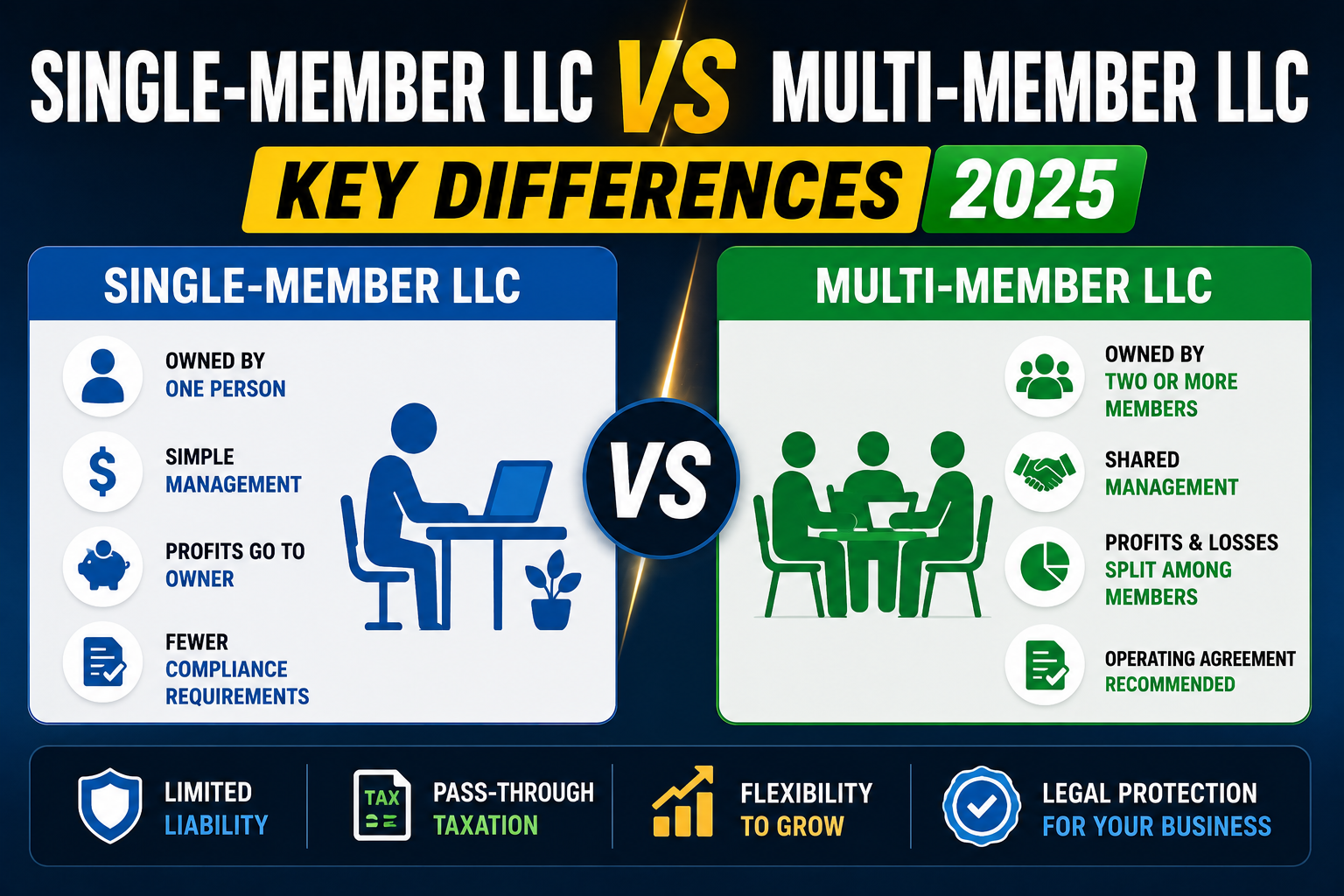

Single-Member LLC vs Multi-Member LLC: Key Differences 2025

1 — Owner required for a single-member LLC — the simplest business structure available

2+ — Owners required for a multi-member LLC — taxed as a partnership by default

$0 — Additional cost to add a member to an LLC — just amend your operating agreement

Schedule C — Tax form used by single-member LLC owners (disregarded entity treatment)

Form 1065 — Annual partnership return required for multi-member LLCs with the IRS

The Core Difference

A single-member LLC has one owner. A multi-member LLC has two or more owners (called members). The structural difference seems simple, but it affects taxation, governance, banking, and the level of documentation you need to maintain. Choosing correctly from the start saves you significant administrative headaches later.

Single-Member LLC: The Default Choice for Solo Entrepreneurs

A single-member LLC is the most common structure for freelancers, consultants, online business owners, and solo entrepreneurs. From the IRS’s perspective, it’s a ‘disregarded entity’ — meaning the LLC itself doesn’t file a separate federal tax return. All income and expenses flow to your personal Form 1040 via Schedule C, exactly as if you were a sole proprietor, but with the liability protection of an LLC.

Key advantages of single-member: simpler taxes (no partnership return), easier banking and account management, complete control over all business decisions without requiring member consent, and simpler operating agreement (or sometimes no formal operating agreement required at all in some states).

Multi-Member LLC: For Two or More Founders

A multi-member LLC is taxed as a partnership by default, meaning the LLC files Form 1065 (Partnership Return) annually with the IRS, and each member receives a K-1 form showing their share of income, losses, and deductions. Each member then reports their K-1 figures on their personal tax returns. The LLC itself pays no federal income tax — it’s still a ‘pass-through’ entity.

Multi-member LLCs require a strong operating agreement that specifies: each member’s ownership percentage, profit and loss distribution (can differ from ownership %), voting rights and decision-making authority, procedures for adding or removing members, and what happens when a member wants to exit.

| Factor | Single-Member LLC | Multi-Member LLC |

|---|---|---|

| Federal tax return | Schedule C (personal return) | Form 1065 (partnership return) + K-1s |

| Tax complexity | Low — integrates with personal taxes | Higher — requires partnership accounting |

| Decision making | Complete sole control | Per operating agreement (can be equal or proportional) |

| Operating agreement | Recommended but simple | Essential and detailed — protects all members |

| Self-employment tax | 15.3% on all net profit | 15.3% on each member’s allocated share |

| S-Corp election | Available — saves SE tax at $40K+ profit | Available — but more complex with multiple members |

The Most Important Consideration: The Operating Agreement

For multi-member LLCs, the operating agreement is the most critical document you’ll create. Without a comprehensive operating agreement specifying what happens when things go wrong — a co-founder wants out, someone wants to bring in investors, a member isn’t contributing their share — you’re exposed to expensive disputes that state default rules will resolve in ways you may not like.

The four most important provisions in a multi-member operating agreement: (1) ownership percentages and how they can change, (2) profit distribution schedule and how distributions are approved, (3) voting thresholds for major decisions (unanimous vs. majority vs. supermajority), (4) member departure and buyout procedures including valuation method.

For operating agreement templates and guidance: LLC Operating Agreement: Free Template and Complete Guide | For formation steps: How to Start an LLC in 2025 for Under $50

Frequently Asked Questions

Can I convert a single-member LLC to multi-member later?

Yes — you amend your Articles of Organization (or file an amendment with your state), add the new member to your operating agreement, and update your EIN information with the IRS. The tax treatment changes when you add a member: you go from disregarded entity (Schedule C) to partnership (Form 1065) for the year the new member joins.

Can a husband and wife form a single-member LLC together?

In community property states, a married couple can elect to treat their jointly owned LLC as a disregarded entity (single-member treatment) for tax purposes, allowing them to use Schedule C instead of Form 1065. In non-community property states, a married couple LLC is generally treated as a multi-member LLC. Check your specific state’s rules.

What if my co-founder and I have an equal 50/50 split — is that wise?

50/50 splits create deadlock risk when co-founders disagree. Consider 51/49 splits to give one person final decision authority, or build explicit deadlock resolution procedures into your operating agreement (mandatory mediation, buyout triggers, etc.). Many successful partnerships use 50/50 ownership with a clear tie-breaking mechanism defined in writing.

Does a multi-member LLC need a separate business bank account?

Yes — absolutely. This is even more critical for multi-member LLCs than single-member. All member contributions, distributions, and business expenses must flow through the business account to maintain proper books. Mixing funds in a multi-member LLC creates both tax nightmares and potential liability exposure.

Can members of a multi-member LLC have different profit splits from their ownership %?

Yes — this is called a ‘special allocation’ and is perfectly legal and common. Example: Two co-founders own 50/50, but one co-founder invested more capital, so they receive 70% of profits for the first 3 years until their additional investment is recouped. These arrangements must be clearly documented in the operating agreement.

Do multi-member LLC members pay self-employment tax?

Yes — members of a multi-member LLC who are active in the business pay self-employment (SE) tax at 15.3% on their share of business income. Passive investors who don’t actively participate in the business may not owe SE tax on their distributions. This is an area where a CPA’s guidance is worth the cost.

Choose the Structure That Fits Your Reality

If you’re a solo entrepreneur, single-member is almost always right — maximum simplicity, minimum compliance burden. If you’re starting with a business partner, multi-member is required — and investing in a well-drafted operating agreement before you need it is the single highest-ROI legal expense you’ll make in your business life.