LLC vs Sole Proprietorship: Which Business Structure Should You Choose in 2026?

Every business owner operating without a formal legal structure is automatically a sole proprietor. It requires no paperwork, no fees, and no registration — which is both its biggest appeal and its most dangerous characteristic. Understanding what you gain by forming an LLC versus staying a sole proprietor is one of the most important business decisions you’ll make. This guide gives you an honest, complete comparison so you can choose with confidence.

How a Sole Proprietorship Works

A sole proprietorship is the default structure for any individual doing business. You don’t file any formation documents — the moment you start earning money from a business activity, you’re legally a sole proprietor. Business income and expenses go on Schedule C of your personal tax return. You and the business are legally the same entity.

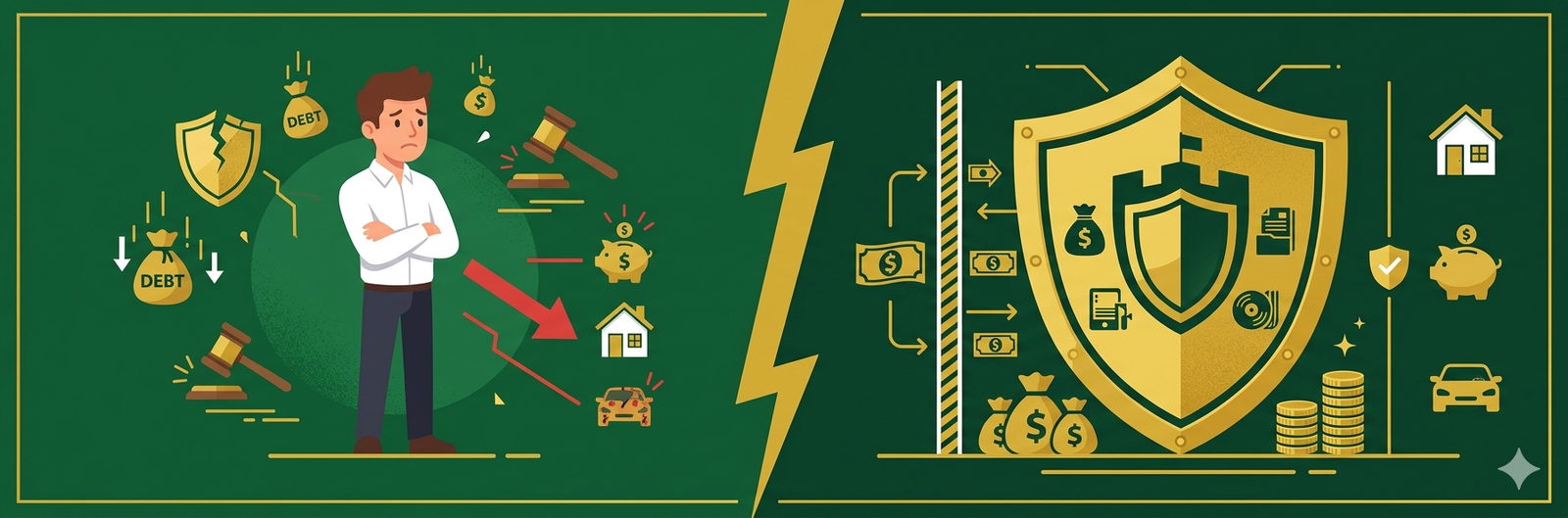

The critical implication: there is no legal separation between you and your business. If your business is sued, your personal assets are at risk. If your business incurs debts it can’t pay, creditors can come after your personal bank accounts, home, and car. This unlimited personal liability is the defining limitation of sole proprietorship.

How an LLC’s Liability Protection Works

An LLC creates a legal separation between you and your business. The LLC is a distinct legal entity — it can own assets, enter contracts, and be sued in its own name. When the LLC is sued or incurs debt, creditors can generally only pursue the LLC’s assets, not your personal assets. This protection is called the “corporate veil.”

Important caveat: the corporate veil can be pierced if you: commingle personal and business funds, fail to maintain the LLC as a separate entity, engage in fraudulent conduct through the LLC, or personally guarantee business debts. Maintaining separation — separate bank account, separate finances, acting through the LLC — is essential for the protection to hold.

The Comprehensive Comparison

| Factor | Sole Proprietorship | LLC |

|---|---|---|

| Formation cost | $0 | $50–$500 (state filing fee) |

| Personal liability | Unlimited — personal assets at risk | Limited — personal assets protected |

| Tax treatment | Schedule C (pass-through) | Pass-through by default; S-corp election available |

| Self-employment tax | 15.3% on all net profit | 15.3% on all profit (without S-corp election); potential savings with S-corp |

| Ongoing requirements | None formal | Annual report + fee; maintain separation |

| Business bank account | Optional but recommended | Essential (required for protection) |

| Credibility | Lower (perceived as informal) | Higher (recognized legal entity) |

| Raising outside investment | Very difficult | Possible (with investor-friendly terms) |

The Tax Dimension: Is There a Difference?

In default configuration — without any special elections — a single-member LLC and a sole proprietorship have nearly identical tax treatment. Both report income and expenses on Schedule C. Both pay 15.3% self-employment tax on net profit. Both are pass-through entities where business income appears on your personal return.

The difference emerges when an LLC makes an S-corporation tax election. At approximately $40,000–$50,000 in annual net profit, the S-corp election can save meaningful amounts in self-employment tax by splitting income between a “reasonable salary” (subject to payroll taxes) and a “distribution” (not subject to self-employment tax). This is the most significant tax benefit of the LLC structure that a sole proprietorship cannot access. For the detailed analysis, see our guide on LLC taxes explained.

When a Sole Proprietorship Is Acceptable

Sole proprietorship is appropriate when:

- You’re testing a business idea before committing to the administrative overhead of an LLC

- Your business has genuinely minimal liability exposure (low-risk services, no employees, no physical location)

- Net profit is under $20,000/year (the tax savings and administrative cost of an LLC may not be worth it at very low income levels)

- You plan to form an LLC once you have consistent revenue

It’s worth emphasizing: “minimal liability exposure” is subjective and frequently wrong. Freelance designers, writers, consultants, and online sellers often assume they have low liability risk until a client dispute, product defect, or intellectual property claim changes that assumption very expensively.

When You Should Definitely Form an LLC

- You have or expect significant revenue (over $40,000 net profit annually)

- Your business involves any potential physical injury to customers or their property

- You have employees or contractors working for you

- You’re signing commercial leases, significant contracts, or taking on debt

- You’re selling physical products (product liability exposure)

- You have meaningful personal assets to protect (home equity, savings, retirement accounts)

- You want to appear credible to large clients, banks, or investors

Real Example: The Cost of Skipping an LLC

Situation: Jennifer, a freelance event planner, operated as a sole proprietor for 3 years. At a corporate event she managed, a catering vendor she contracted was involved in a food safety incident that hospitalized 4 attendees. The corporate client sued both the caterer and Jennifer personally — because she was the contracting party with both the client and the vendor as a sole proprietor.

Result: Jennifer’s homeowner’s insurance partially covered the claim, but she faced $80,000 in uninsured legal costs and a partial judgment against her personal assets. She settled for $45,000 from personal funds.

If she had formed an LLC: The lawsuit would have been against Jennifer’s LLC, not Jennifer personally. The LLC had no significant assets (she hadn’t built up business equity). Her personal home and savings would not have been at risk.

Cost of forming an LLC in her state: $125.

Converting From Sole Proprietorship to LLC

Converting is straightforward and can be done at any time:

- Form the LLC through your state Secretary of State (see our LLC formation guide)

- Obtain a new EIN for the LLC

- Open a business bank account in the LLC’s name

- Update contracts, licenses, and business relationships to reflect the new entity

- Transfer any business assets to the LLC (typically a simple written transfer document)

- Notify existing clients and vendors of the name change

There’s no filing required with the IRS to “convert” — your old Schedule C simply ends and the LLC begins filing under its new EIN.

Frequently Asked Questions

Can a sole proprietor use a business name (DBA)?

Yes — a “Doing Business As” (DBA) or fictitious business name registration allows a sole proprietor to operate under a trade name. However, a DBA provides no liability protection — you’re still personally responsible for all business obligations. It’s often confused with business entity formation; they are completely different things.

Does an LLC protect me from everything?

No. LLC protection has limits: you remain personally liable for your own professional negligence (a doctor’s LLC doesn’t protect against malpractice committed personally), for personal guarantees you sign, for payroll taxes, and in cases where courts pierce the corporate veil. Professional liability insurance is important alongside, not instead of, LLC formation.

Is forming an LLC complicated for a freelancer?

Not in most states. The filing is a 20-minute online process at your state’s Secretary of State website. The main ongoing requirement is maintaining separation between personal and business finances — which most professionals should be doing anyway for bookkeeping purposes. See our complete walkthrough in how to form an LLC.

Conclusion

For the vast majority of small business owners making more than $25,000 annually or operating in any context where liability is possible, the LLC is clearly superior to sole proprietorship. The $50–$300 formation cost and minimal ongoing administrative requirements provide personal asset protection worth infinitely more than the cost. The question isn’t really whether an LLC is worth it — it is. The question is whether to form one now or wait, and for most active businesses, the answer is now. The risk of operating unprotected increases every day your business grows.

Stop Operating Unprotected

Free LLC vs Sole Proprietorship decision worksheet — find your ideal structure in 5 minutes.