LLC Taxes Explained: Complete Guide for Small Business Owners

LLC taxation confuses many new business owners because LLCs are not taxed at the entity level by default — instead, income passes through to the owners who pay tax on their personal returns. This guide explains exactly how LLCs are taxed, the S-Corp election strategy, quarterly estimated taxes, and the most important deductions for LLC owners.

Disclaimer: This content is for educational purposes only and does not constitute tax advice. Tax laws change and vary by situation. Always consult a qualified CPA or tax attorney for advice specific to your business.

Default LLC Tax Treatment

Single-member LLC: Treated as a disregarded entity. All income and deductions reported on Schedule C of your personal Form 1040. Self-employment tax of 15.3% applies to net profits (12.4% Social Security + 2.9% Medicare). Federal income tax applies at your personal rate.

Multi-member LLC: Treated as a partnership. LLC files Form 1065 (informational return) and issues K-1s to each member. Each member reports their share of income on their personal return and pays self-employment tax. Read What is an LLC? for foundational context.

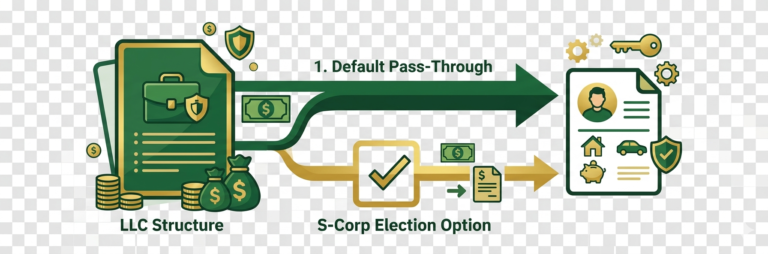

The S-Corp Election: How to Save on Self-Employment Tax

An LLC can elect to be taxed as an S-Corporation by filing Form 2553 with the IRS. This election allows the owner to split income into two components: a reasonable salary (subject to payroll taxes) and a distribution (not subject to self-employment tax). At net profit levels above approximately $40,000 to $60,000, the self-employment tax savings can exceed the additional accounting costs. Example: $100,000 net profit. Default LLC: pay SE tax on entire $100,000 = approximately $14,130 in SE tax. S-Corp election with $60,000 salary: pay SE tax only on $60,000 = approximately $8,478 in SE tax. Savings: approximately $5,652 annually. This strategy requires paying yourself a reasonable salary, running payroll, and filing additional tax returns — typically requiring a CPA.

Quarterly Estimated Tax Payments

As an LLC owner, no employer withholds taxes from your income. You are responsible for paying taxes throughout the year through quarterly estimated payments due in April, June, September, and January. Failing to make adequate estimated payments results in underpayment penalties from the IRS. A safe harbor rule: paying 100% of last year’s tax liability (or 110% for high earners) avoids underpayment penalties.

Key LLC Tax Deductions

Home office deduction (if you use dedicated space exclusively for business), business vehicle expenses, health insurance premiums, retirement plan contributions, business equipment and software, professional services (legal, accounting), business travel, education and professional development, and the 20% qualified business income (QBI) deduction. Work with a CPA to ensure you claim all legitimate deductions.

State LLC Taxes

Beyond federal taxes, most states also tax LLC income at the state level. California charges an $800 minimum franchise tax plus an additional fee based on gross receipts over $250,000. Other states have their own rates and rules. Your CPA can help you understand your state-specific obligations.

Conclusion

LLC taxation is manageable with basic understanding and good record-keeping. Work with a qualified CPA — the cost of professional tax guidance is almost always worth it for LLC owners. Continue with How to Get an EIN for Your LLC and LLC Bank Account Setup.